Chapter 13 - Regression

13.1 The Basics of Regression

Regression is the most common way in which we fit a line to explain variation. Using one variable to explain variation in another is a key part of what we’ve been doing the whole book so far!

When it comes to identifying causal effects, regression is the most common way of estimating the relationship between two variables while controlling for others, allowing you to close back doors with those controls.197 Saying we “adjust” for those variables, rather than control for them, is probably more accurate, since we don’t actually have control of anything here as we would in a controlled experiment. But “control” is the most common way of saying it. Naturally it’s relevant to what we’re doing. Not only will we be discussing it further in this chapter, but many of the methods described in other chapters of Part II of the book are themselves based on regression.

We’ve already covered the basics of regression, back in Chapter 4. So go back and take a look at that.

Some key points from that chapter:

- We can use the values of one variable (\(X\)) to predict the values of another (\(Y\)). We call this explaining \(Y\) using \(X\).198 This is a purely statistical form of “explanation.” It’s not an explanation why \(Y\) happens (unless we’ve identified the effect of \(X\) on \(Y\)), just the ability to predict \(Y\) using \(X\).

- While there are many ways to do this, one is to fit a line or shape that describes the relationship. For example, \(Y = \beta_0 + \beta_1X\). Estimating this line using ordinary least squares (standard, linear regression) will select the line that minimizes the sum of squared residuals, which is what you get if you take the prediction errors from the line, square them, and add them up. Linear regression, for example, gives us the best linear approximation of the relationship between \(X\) and \(Y\). The quality of that approximation depends in part on how linear the true model is.

- Pro: Uses variation efficiently

- Pro: A shape is easy to explain

- Con: We lose some interesting variation

- Con: If we pick a shape that’s wrong for the relationship, our results will be bad

- We can interpret the coefficient that multiplies a variable (\(\beta_1\)) as a slope. So, a one-unit increase in \(X\) is associated with a \(\beta_1\) increase in \(Y\).

- With only one predictor, the estimate of the slope is the covariance of \(X\) and \(Y\) divided by the variance of \(X\). With more than one, the result is sort of similar, but also it accounts for the way the different predictors are correlated.

- If we plug an observation’s predictor variables into an estimated regression, we get a prediction \(\hat{Y}\). This is the part of \(Y\) that is explained by the regression. The difference between \(Y\) and \(\hat{Y}\) is the unexplained part, which is also called the “residual.”

- If we add another variable to the regression equation, such as \(Y = \beta_0 + \beta_1X+ \beta_2Z\), then the coefficient on each variable will be estimated using the variation that remains after removing what is explained by the other variable. So our estimate of \(\beta_1\) would not give the best-fit line between \(Y\) and \(X\), but rather between the part of \(Y\) not explained by \(Z\) and the part of \(X\) not explained by \(Z\). This “controls for \(Z\).”

- If we think the relationship between \(Y\) and \(X\) isn’t well-explained by a straight line, we can use a curvy one instead. Ordinary least squares (OLS) can handle things like \(Y = \beta_0+ \beta_1X + \beta_2X^2\) that are “linear in parameters” (notice that the parameters \(\beta_1\) and \(\beta_2\) are just plain multiplied by a variable, then added up), or we can use nonlinear regression like probit, logit, or a zillion other options.

Those are the basics that more or less explain how regression works. And as long as that regression model looks like the population model (the true relationship is well-described by the shape we choose), it has a good chance of working pretty well. But there’s still plenty left to cover. What else do we need to know?

We’re going to add a few pieces of OLS that we haven’t covered yet, or at least not thoroughly:

- The error term

- Sampling variation

- The statistical properties of OLS

- Interpreting regression results

- Interpreting coefficients on binary and transformed variables

That’s a lot to get through! Let’s get going.

13.1.1 Error Terms

Residual. The difference between a prediction and the actual outcome.

Error. The difference between the actual outcome and prediction we’d make if we had infinite observations to estimate our prediction.

A lot of the detail of regression is hidden in the places it doesn’t go. I previously described fitting a straight line as figuring out the appropriate \(\beta_0\) and \(\beta_1\) values to give us the line \(Y = \beta_0 + \beta_1X\).

However, in our actual data, that line is clearly insufficient. It will rarely predict any observation perfectly, much less all of the observations. There’s going to be a difference between the line that we fit and the observation we get. That’s what I mean by “the places it doesn’t go.” We can add this difference to our actual equation as an “error term” which I’ll mark as \(\varepsilon\). So now our equation is:

That difference goes by two names: the residual, which we’ve talked about, is the difference between the prediction we make with our fitted line and the actual value, and the error is the difference between the true best fit-line and the actual value. Why the distinction? Well… sampling variation. Because we only have a finite sample, the best-fit line we get with the data we have won’t quite be the same as the best-fit line we’d get if we had data on the whole population.199 Remember Chapter 3? All we can really see will be the residual, but we need to keep that error in mind. As we know from Chapter 3, we want to describe the population. Those population-level errors will help us figure out what’s going on.

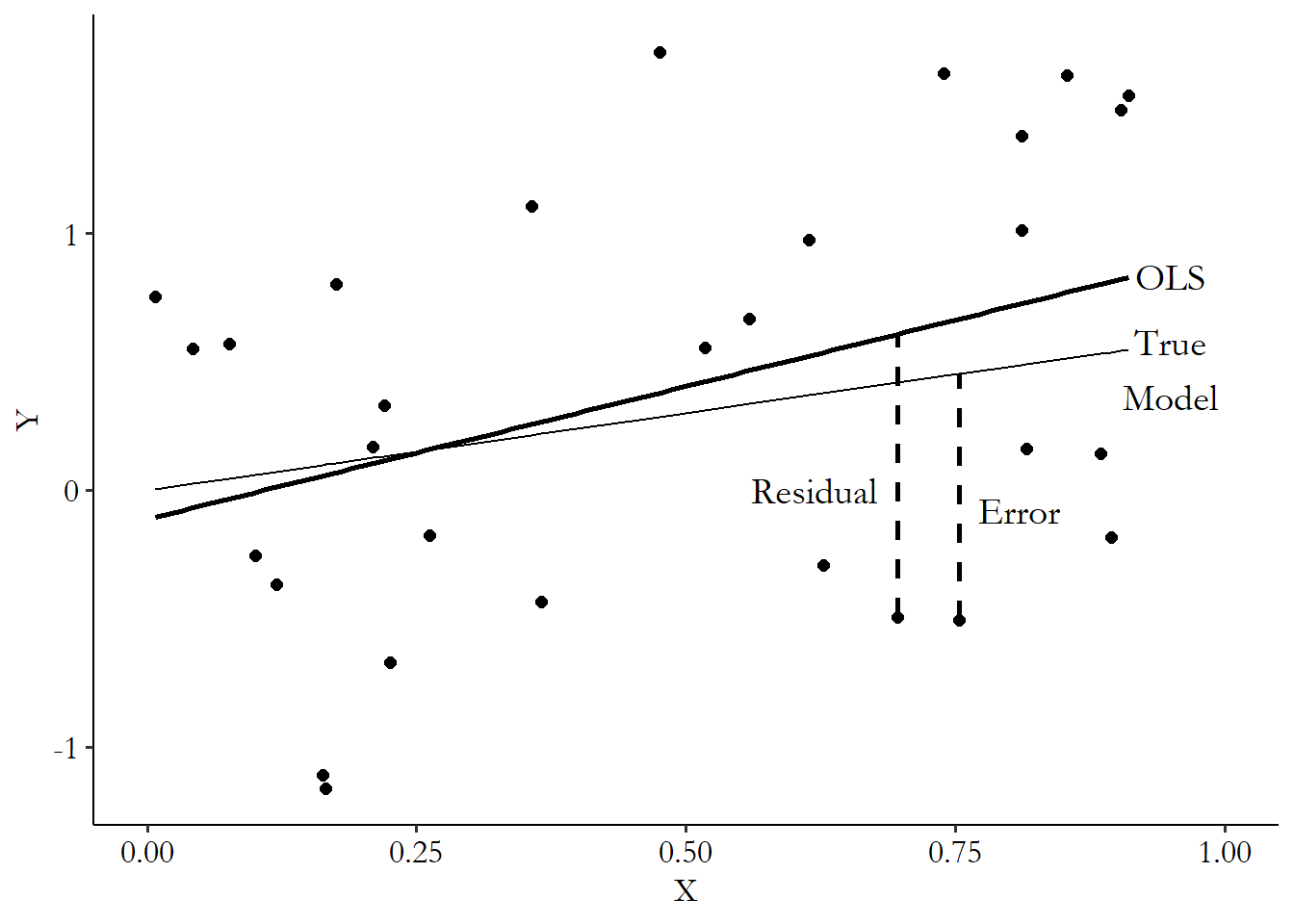

You can see the difference between a residual and an error in Figure 13.1. The two lines on the graph represent the true model that I used to generate the data in the first place, and the OLS best-fit line I estimated using the randomly-generated sample. For each point, the vertical distance from that point to the OLS line is the residual (since the OLS line represents our prediction), and the vertical distance from that point to the true model is the error (since even if we knew the true model relating \(Y\) and \(X\), we still wouldn’t predict the point perfectly because of the other stuff that goes into \(Y\)).

Figure 13.1: The Difference Between the Residual and the Error

So what’s in an error, anyway? Where does it come from? Well, the error effectively contains everything that causes \(Y\) that is not included in the model. \(Y\) is on the left-hand-side of the \(Y = \beta_0 + \beta_1X + \beta_2Z + \varepsilon\) equation, and it’s determined by the right-hand-side. So if there’s something that goes into \(Y\) but isn’t \(X\) or \(Z\), then it has to come from somewhere. That somewhere is \(\varepsilon\).

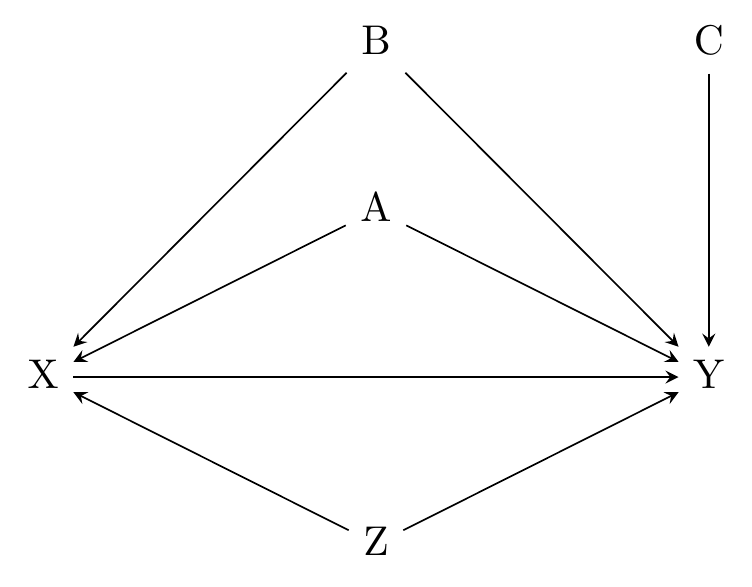

\(\varepsilon\) includes both stuff we can see and stuff we can’t. So, for example, if the true model is given by Figure 13.2, and we are using the OLS model \(Y = \beta_0 + \beta_1X + \beta_2Z + \varepsilon\), then \(\varepsilon\) is made up of some combination of \(A\), \(B\), and \(C\). We know that since we can determine from the graph that \(A\), \(B\), and \(C\) all cause \(Y\), but they aren’t in the model.

Figure 13.2: Depending on the Model Used, A, B, C, and Z Might Be in the Error Term

13.1.2 Regression Assumptions and Sampling Variation

Thinking about what’s in the error term leads us to the first assumption we’ll need to make about the error term. There are going to be a few of these assumptions, and I’ll bring them up as they become necessary. People who use regression tend to be obsessed about those lil’ \(\varepsilon\)s and the assumptions we make about them. Go to any research seminar, and you’ll hear endless questions about error terms and whether the assumptions we need to make about them are likely to be true.

Exogeneity assumption. In a regression context, the assumption that the variables in the model (or perhaps just our treatment variable) are uncorrelated with the error term.

The first assumption we’ll talk about links the first and second parts of the book, and it’s the exogeneity assumption. If we want to say that our OLS estimates of \(\beta_1\) will, on average, give us the population \(\beta_1\), then it must be the case that \(X\) is uncorrelated with \(\varepsilon\).200 Oddly, this does not require that \(X\) and \(\varepsilon\) are completely unrelated, just uncorrelated - there can be a relationship between the two, just not a linear relationship. For example, if the relationship between \(X\) and \(\varepsilon\) looks like a V or a U, then they’re clearly related, but a straight line describing the relationship would be flat. The downward part would cancel out with the upward part. In reality, it’s pretty rare that two variables are related but completely uncorrelated, so this doesn’t usually let us get away with ignoring a relationship between \(X\) and \(\varepsilon\).

If that sounds familiar, it’s because we’re really just restating the conditions for identifying a causal effect! Every variable that causes \(Y\) in a causal diagram like Figure 13.2 ends up in the regression equation somehow, whether it’s one of the variables in the model or just in \(\varepsilon\). If a variable is in the regression equation directly, then that closes any causal paths that go through that variable. By adding a variable to the regression, we “control for it” or “add it as a control.” So with the regression \(Y = \beta_0 + \beta_1X + \beta_2Z + \varepsilon\), the path \(X \leftarrow Z \rightarrow Y\) is closed.

But if something is still in the error term and is correlated with \(X\), we haven’t closed the path. Since \(A\) is in \(\varepsilon\), and we know from the diagram that \(A \rightarrow X\), then we can say either that (a) we haven’t closed the \(X \leftarrow A \rightarrow Y\) back door path, and so the effect of \(X\) isn’t identified, or, (b) \(X\) is correlated with \(\varepsilon\) and so is “endogenous” rather than exogenous, and the effect of \(X\) isn’t identified.201 The terms “endogeneity” and “exogeneity” come from the biology terms “endogeny” and “exogeny,” which roughly mean “from within the system” and “from outside the system.” Endogenous variables are determined by other things in the system (other things that are part of determining the outcome). These are saying, in effect, the same thing, just using lingo from different domains.202 There are yet other ways to talk about this in other fields. You could also say that \(A\) is an “unobserved/unmeasured confounder” or that \(X\) and \(Y\) have a “spurious correlation.”

Similarly, we can say in either set of lingo that we don’t need to worry about \(C\) being in our model. It’s in the error term - everything that predicts \(Y\) but isn’t in the model is in the error term. But we can say either (a) there’s no back door from \(X\) to \(Y\) that goes through \(C\), or (b) \(X\) is unrelated to \(C\) and so \(C\) isn’t leading \(X\) to be endogenous.

Bias. An estimate that, on average, gives the wrong answer, no matter how big your sample size gets, is biased.

Omitted variable bias. Bias in a regression estimate that occurs because a variable correlated with the treatment is in the error term and otherwise omitted from the model.

Speaking of lingo, if we do have that endogeneity problem, then on average our estimate of \(\beta_1\) won’t give us the population value. When that happens - when our estimate on average gives us the wrong answer, we call that a bias in our estimate. In particular, this form of bias, where we are biased because a variable correlated with \(X\) is in the error term, is known as omitted variable bias, since it happens because we omitted an important variable from the regression equation. Previously in the book we’d say we failed to close the back door that goes through \(A\). In this lingo, we’d say that \(A\) gave us omitted variable bias, but \(C\) doesn’t.

So that’s our first assumption about the error term - the exogeneity assumption, that \(\varepsilon\) is uncorrelated with any variable we want to know the causal effect of. We know how to think about whether that assumption is true - the entire first half of this book is about figuring out what’s necessary to identify a causal effect.

Of course, that’s only the first thing we need to assume about the error term. Many of the others, though, relate to the sampling variation of the OLS estimates.

Just like the means we discussed in Chapter 3, regression coefficients are estimates, and even though there’s a true population model out there, the estimate we get varies from sample to sample due to sampling variation.

Conveniently, we have a good idea what that sampling variation looks like. We know that we can think of observations as being pulled from theoretical distributions. We also know that statistics like the mean can also be thought of as being pulled from theoretical distributions. In the case of the mean, that’s a normal distribution (see Chapter 3). If you drew a whole bunch of samples of the population and took the mean each time, the distribution of means across the sample would follow a normal distribution. Then we can use the estimated mean we get to try to figure out what the population mean is.

Regression coefficients also follow a normal distribution, and we know what the mean and standard deviation of that normal distribution is. Or, at least we do if we make a few more assumptions about the error term.

What is that normal distribution that the OLS coefficients follow?203 The following calculations will assume that the exogeneity assumption mentioned earlier holds.

In a regression model with one predictor, like \(Y = \beta_0 + \beta_1X + \varepsilon\), an OLS estimate \(\hat{\beta}_1\) of the true-model population \(\beta_1\) follows a normal distribution with a mean of \(\beta_1\) and a standard deviation of \(\sqrt{\sigma^2/(var(X)n)}\), where \(n\) is the number of observations in the data, \(\sigma\) is the standard deviation of the error term \(\varepsilon\), and \(var(X)\) is the variance of \(X\).204 Wait, how do we get the standard deviation of \(\varepsilon\) if we can’t see it? Well, we don’t know it exactly, so our idea of this sampling distribution will itself be an estimate based on our best guess of \(\sigma\). We use the residual, which we can see, instead of the error, and base our estimate of \(\sigma\) on the standard deviation of the residual. This standard deviation isn’t generally called a standard deviation, though. The standard deviation of a sampling distribution is often referred to as a standard error. And that’s what we’ll call them here too.

Standard error. The standard deviation of a sampling distribution.

If there’s more than one variable in the model, the math starts to require matrix algebra, but it’s the same idea. In the regression model \(Y = \beta_0 + \beta_1X+ \beta_2Z + \varepsilon\), the OLS estimates \(\hat{\beta}_1\) and \(\hat{\beta}_2\) follow a joint normal distribution, where their respective means are the population \(\beta_1\) and \(\beta_2\), and the standard deviations are the square roots of the diagonal of \(\sigma^2(A'A)^{-1}/n\), where \(A\) is a two-column matrix containing both \(X\) and \(Z\). But you can think of \((A'A)^{-1}\) as saying “divide by the variances and covariances of \(X\) and \(Z\),” just like \(\sqrt{\sigma^2/(var(X)n)}\) says “divide by the variance of \(X\).”

How can we make an OLS estimate’s sampling variation really small? There are only three terms in the standard deviation, so only three things to change: (1) We could shrink the standard deviation of the error term \(\sigma\), i.e., make the model predict \(Y\) more accurately, (2) we could pick an \(X\) that varies a lot and has a big variation - an \(X\) that changes a lot makes it easier to check whether \(Y\) is changing at the same time, or (3) we could use a big sample so \(n\) gets big.

How about those other assumptions we need to make about the error term? It turns out that those assumptions are necessary to assume that the stuff I’ve said up to now about the standard error is true. Let’s tuck that away in our back pocket for now and ignore that looming problem. We’ll come back to it in the “Your Standard Errors are Probably Wrong” section below. All of the things I’m going to say now about using standard errors will still hold up. There might just need to be some minor adjustments to the way we calculate them, which is what we’ll discuss in that section.

13.1.3 Hypothesis Testing in OLS

Okay, so why did we want to know the OLS coefficient distribution again? The same reason we want to think about any theoretical distribution - theoretical distributions let us use what we observe to come to the conclusion that certain theoretical distributions are unlikely.

And since the theoretical distribution of our OLS estimate \(\hat{\beta}_1\) is centered around the population parameter \(\beta_1\), that means we can use our estimate \(\hat{\beta}_1\) to say that certain population parameters are very unlikely, for example “it’s unlikely that the effect of \(X\) on \(Y\) is 13.2.”

To recap what we’re doing here, modifying only slightly what we have from Chapter 3:

- We pick a theoretical distribution, specifically a normal distribution centered around a particular value of \(\beta_1\)

- Estimate \(\beta_1\) using OLS in our observed data, getting \(\hat{\beta}_1\)

- Use that theoretical distribution to see how unlikely it would be to get \(\hat{\beta}_1\) if indeed the true population value is what we picked in the first step

- If it’s super unlikely, that initial value we picked is probably wrong!205 Or, if you’re Bayesian, that initial value needs to be revised a lot.

We can take this a step further towards the concept of hypothesis testing. Hypothesis testing is a way of formalizing the four steps above into a way of making a decision about whether we can “reject” the theoretical distribution, and thus the original \(\beta_1\) we picked.206 There are plenty of reasons not to like hypothesis testing, but it’s extremely common, and so you have to know about it to figure out what’s going on. What’s wrong with it? It depends on the arbitrary and strangely sharp choice of rejection value (\(p = .049\) rejects the null, but \(p = .051\) doesn’t?), and it also relies on the idea that you’ve “found a result” when you’ve really just rejected something obviously false. In social science, very few relationships are truly exactly zero, and yet that’s almost always our null-hypothesis value. So with enough sample size we always reject the null. My opinion: use significance testing; it is useful and it helps you converse with other people doing research. But don’t get too serious about it. And certainly never choose your model based on significance! The first half of this book is about much better ways to choose models.

Under hypothesis testing, we pick a “null hypothesis” - the initial \(\beta_1\) value we’re going to check against. In practice, this is almost always zero (although it certainly doesn’t have to be), so let’s simplify and say that our null hypothesis is \(\beta_1 = 0\).

Then, we pick a “rejection value” \(\alpha\). If we calculate that the probability of getting our estimated result from the theoretical distribution based on \(\beta_1 = 0\) is below \(\alpha\), then we say that’s too unlikely, and conclude that \(\beta_1 = 0\) is false, rejecting it. Commonly, this rejection value is \(\alpha = .05\), so if the estimate we get (or something even stranger) has a 5% chance or less of occurring if the null value is true, then we reject the null.

Once we’ve rejected \(\beta_1 = 0\), what conclusion can we come to? Not that our estimate is correct - we certainly don’t know that; there are plenty of nonzero values we haven’t rejected. All we can say is that we don’t think it’s likely to be 0. Knowing it’s not zero can be handy - if it’s not zero, that means there’s some relationship there. And that’s our conclusion.

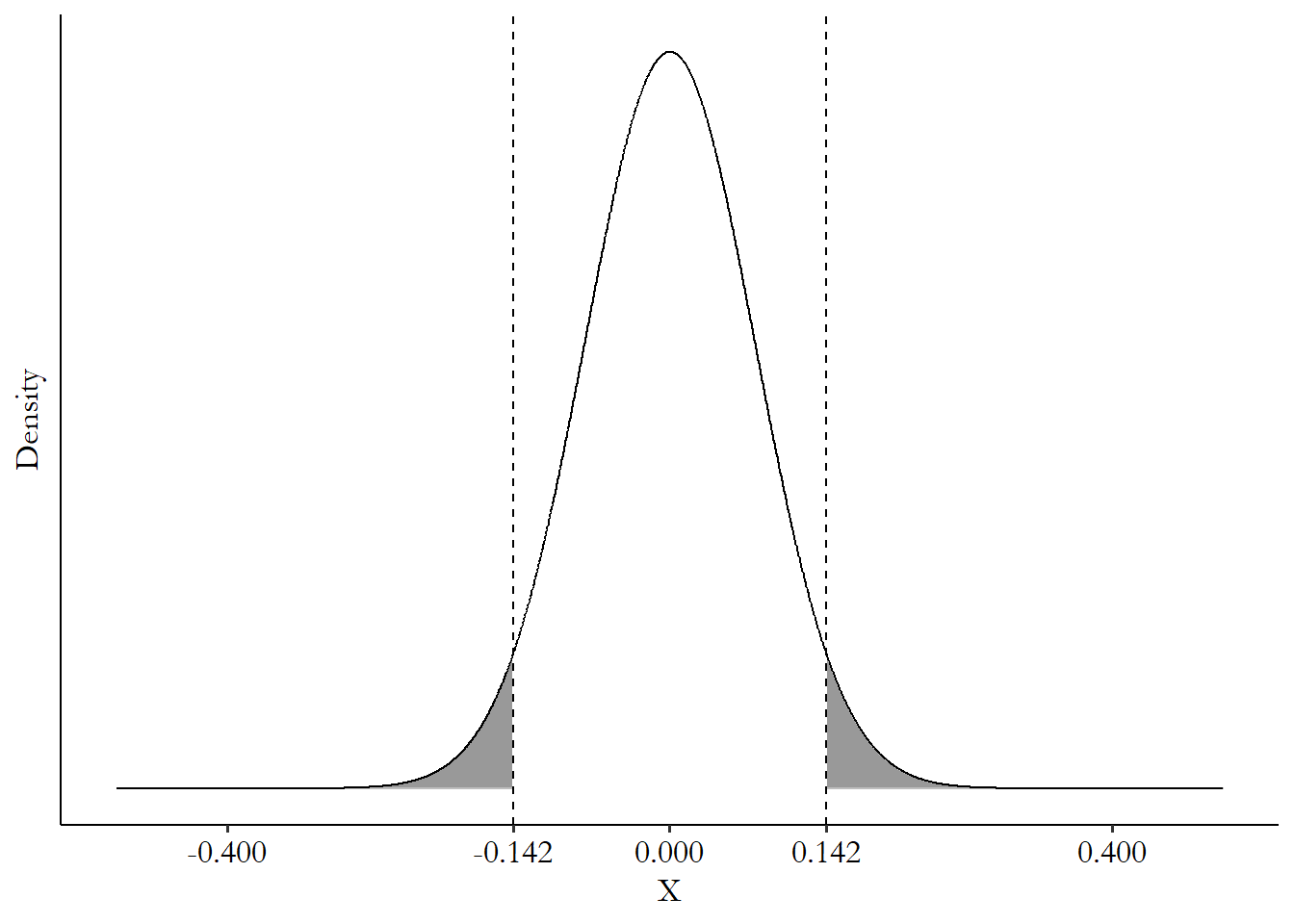

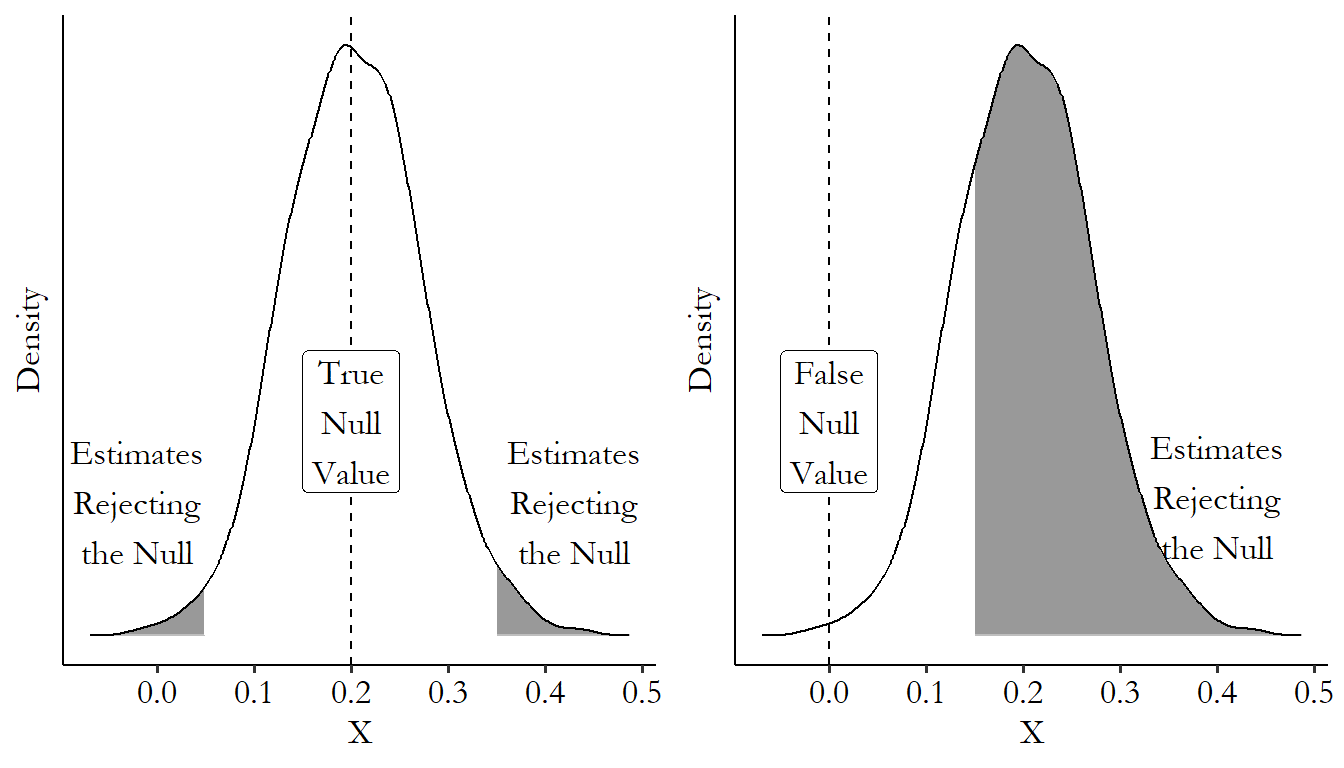

To see this in action, I generated 200 random observations using the true model \(Y = 3 + .2X + \varepsilon\), where \(\varepsilon\) is normally distributed with mean 0 and variance 1. Then, pretending that we don’t know the truth is \(\beta_1 = .2\), I estimated the OLS model using the regression \(Y = \beta_0 + \beta_1X + \varepsilon\).

The first estimate I get is \(\hat{\beta_1} = .142\). I can use the formula from the last section to also calculate that the standard error of \(\beta_1\) is \(se(\beta_1) = .077\). So the theoretical distribution I’m looking at is a normal distribution with mean 0 and standard deviation \(.077\).

Under that distribution, the \(.142\) estimate I got is at the 96.7th percentile of the theoretical distribution, as shown in Figure 13.3. That means that something as far from 0 as \(.142\) is (or farther) happens \((100 - 96.7)\times 2 = 3.3\times2 =\) 6.6% of the time.207 Note I’ve doubled the percentile here - that’s because “as far away or farther” includes both sides of the distribution. This is a “two-tailed test,” which is standard. If we did a “one-tailed test,” caring only if it was as far away or farther in the same direction, we wouldn’t do the doubling. If we started with \(\alpha = .05\), then we would not reject the \(\beta_1 = 0\) null hypothesis, since 6.6% is higher than 5%, even though we happen to know for a fact that the null is quite wrong.

Figure 13.3: Comparison of Our .142 Estimate to a Theoretical Null Distribution Centered at 0

We can see how this works from a different angle in Figure 13.4. This time I’m generating a bunch of samples of random data and showing the sampling distribution against a given null value. I’m magically giving myself the knowledge that \(\beta_1 = .2\) is the true value to test against. I generate random data from that same true model \(Y = 3 + .2X + \varepsilon\) a whole bunch of times, estimate \(\hat{\beta}_1\) using OLS, and test it against the null of \(\beta_1 = .2\). Sometimes I still reject the null, even though the null is literally true, but not often. In fact, I reject it exactly 5% of the time, because of the \(\alpha = .05\) decision. Sampling variation will do that! This is a rejection of something that’s true, and how often we do it is the “false positive” rate, or the terribly-named “type I error rate.”208 Why is it a false “positive”? Because we sort of think about hypothesis testing as a “success” when we reject the null. This is silly, of course - we want to find the true value, not just go around rejecting nulls. A well-estimated non-rejection is much more valuable than a rejection of the null from a bad analysis. But there seems to be something in human psychology that makes us not act as though this is true.

I then test those same estimates against the null of \(\beta_1 = 0\). Sometimes I fail to reject the null, even though the null is false. Sampling variation does this too! Our failure to reject false nulls is the “false negative” rate or the “type II error rate.”

What these figures demonstrate is that hypothesis testing really isn’t about pinning down a true value, nor is it about hard-and-fast, true-and-false results. It’s about showing that certain theoretical distributions are unlikely. And we can then say that if they’re too unlikely, we can forget about them.

Figure 13.4: Testing 1,000 Randomly Generated Samples Against the True Null and a False Null

In practice, when applied to regression in most contexts, we’re talking about a normally-distributed regression coefficient and an \(\alpha = .05\) false positive rate (with a two-tailed test), testing against a null that the coefficient is 0. So if the probability of our estimate (or something even farther from 0) occurring is less than 5%, we call that “statistically significant” and say the relationship is nonzero.

The calculation of the probability comes from computing the percentiles of the normal distribution with a mean of 0 and a standard deviation of our estimated \(se(\hat{\beta}_1)\). If our estimate \(\hat{\beta}_1\) is below the 2.5th percentile or above the 97.5th, that’s statistically significant with \(\alpha = .05\).

We can also look at the exact percentile we get and evaluate that. If, for example, we find that our estimate of \(\hat{\beta}_1\) is at the 1.3rd percentile, then we can double that to 2.6, and say that we have a 2.6% probability of being that far away from the null or farther. This probability is called the “p-value.” The lower that p-value is, the lower the chance is of finding a result that far from the null or farther by sampling variation alone. If you look back at Figure 13.3, the entire shaded area is the p-value, since it’s the area as far away from the null as the actual estimate is, or farther. If the p-value is below \(\alpha\), that’s statistical significance.

p-value. The probability of getting an estimated result as far from the null (or farther), given the theoretical sampling distribution based on the chosen null-hypothesis value.

Using some known properties of the normal distribution, we can take a shortcut without having to go to the trouble of calculating percentiles. In this context, the t-statistic is the coefficient divided by its standard error \(\hat{\beta}_1/se(\hat{\beta}_1)\). When we scale the estimate by its standard error, that puts us on the “standard normal” theoretical distribution where the standard deviation is 1. Then, if that t-statistic is below -1.96 (the 2.5th percentile) or above 1.96 (the 97.5th percentile), that’s statistically significant at the 95% level, and a nonzero relationship.

Using that sort of interpretation is what lets us read regression tables, which we’ll get to in a second. But before we do, one aside on this whole concept of statistical significance. Rather, a plea.

Having taught plenty of students in statistical methods, and, further, talked with plenty of people who have received teaching in statistical methods, the single greatest difference between what students are taught and what students learn is about statistical significance. I think this is because significance is wily and tempting.209 If the Lord of the Rings were statistics, significance testing would be the One Ring. Not to mention all the people trying to throw it into a volcano. Of course if Lord of the Rings really were statistics, they wouldn’t have made those movies about it. Powerful, tempting, seemingly simple, but so easy to misuse, and so easy to let it take you over and make you do bad things. So please keep the following things in mind and repeat them as a mantra at every possible moment until they live within you:

- An estimate not being statistically significant doesn’t mean it’s wrong. It just means it’s not statistically significant.

- Never, ever, ever, ever, ever, ever, ever give in to the thought: “oh no, my results aren’t significant, I’d better change the analysis to get something significant.” Bad.210 Why? First off, maybe there truly just isn’t much of an effect. Insignificant doesn’t mean wrong! Also, changing the analysis to seek significance makes your future significance tests incorrect and meaningless - the tests all assume that you don’t do this. Your results become garbage, even if they look nice and you can fool people into thinking they’re good. I’m pretty sure professors always say to never do this, but students somehow remember the opposite.211 To be fair, sometimes researchers do this too. It’s called ``p-hacking,’’ where you keep changing your statistical analysis until you find some way to produce a statistically significant result. It’s bad. It’s a bad thing that is bad when it’s done because it’s bad to do and it makes the results bad. Bad.

- A lot of stuff goes into significance besides just “is the true relationship nonzero or not.” - sampling variation, of course, and also the sample size, the way you’re doing your analysis, your choice of \(\alpha\), and so on. A significance test isn’t the last word on a result.212 That said, speculating on whether an insignificant result would become significant with, say, a bigger sample size generally isn’t too useful.

- Statistical significance only provides information about whether a particular null value is unlikely. It doesn’t say anything about whether the effect you’ve found matters. In other words, “statistically significant” isn’t the same thing as “significant.”213 Even though researchers, myself included, will often just say “significant” as a shorthand for statistically significant. A result showing that your treatment improves IQ by .000000001 points is not a meaningful effect, whether it’s statistically significant or not.

Keep in mind, generally: the point of significance testing is to think about not just the estimates themselves but also the precision of those estimates. If you’ve got a really cool result but the standard errors are huge, there’s a good chance it’s a fluke that could be consistent with lots of true relationships. That’s the kind of thinking significance testing is meant to encourage. But there are other ways to keep precision in mind. You could just think about the standard errors themselves; ask if the estimate is precise regardless of whether it’s far from a given null value. You could ask what the range of reasonable null values is (construct a confidence interval) instead of focus on one in particular. You could go full Bayesian and do whatever the heck it is those crazy cats get up to. Significance testing is just one way of doing it, and it has its pros and cons like everything else.

13.1.4 Regression Tables and Model-Fit Statistics

We have a decent idea at this point of how to think about the line that an OLS estimation produces, as well as the statistical properties of its coefficients. But how can we interpret the model as a whole? How can we make sense of a whole estimated regression at once? For that we can turn to the most common way that regression results are presented: the regression table.

We’re going to run some regressions using data on restaurant and food inspections. We might be curious whether chain restaurants get better health inspections than restaurants with fewer (or only one) location.214 This data comes from Louis-Ashley Camus on Kaggle We’ll be using this data throughout this chapter. Some basic summary statistics for the data are in Table 13.1. We have data on the inspection score (with a maximum score of 100), the year the inspection was performed, and the number of locations that restaurant chain has.

Table 13.1: Summary Statistics for Restaurant Inspection Data

| Variable | N | Mean | Std. Dev. | Min | Pctl. 25 | Pctl. 75 | Max |

|---|---|---|---|---|---|---|---|

| Inspection Score | 27178 | 94 | 6.3 | 66 | 90 | 100 | 100 |

| Year of Inspection | 27178 | 2010 | 5.9 | 2000 | 2006 | 2016 | 2019 |

| Number of Locations | 27178 | 65 | 84 | 1 | 27 | 71 | 646 |

Now I’ll run two regressions. The first just regresses inspection score on the number of locations the chain has:

and the second adds year of inspection as a control:

I then show the estimated results for both in Table 13.2.

| Inspection Score | Inspection Score | |

|---|---|---|

| (Intercept) | 94.866*** | 225.333*** |

| (0.046) | (12.411) | |

| Number of Locations | −0.019*** | −0.019*** |

| (0.000) | (0.000) | |

| Year of Inspection | −0.065*** | |

| (0.006) | ||

| Num.Obs. | 27178 | 27178 |

| R2 | 0.065 | 0.068 |

| R2 Adj. | 0.065 | 0.068 |

| F | 1876.705 | 997.386 |

| RMSE | 6.05 | 6.04 |

| * p < 0.1, ** p < 0.05, *** p < 0.01 |

What can we see in Table 13.2? Each column represents a different regression. The first column of results shows the results from the Equation (13.2) regression, and the second column of results shows the results from the Equation (13.3) regression.

The first thing we notice is that each variable used to predict Inspection Score gets its own set of two rows. The “Intercept” also gets two rows - this is \(\hat{\beta}_0\), and on some tables is called the “Constant.” The first row shows the coefficient estimate. Our estimate \(\hat{\beta}_1\), the coefficient on Number of Locations, is \(\hat{\beta}_1 = -.0019\). It happens to be the same in both regressions - the addition of Year as a control didn’t change the estimate enough to notice. There are also some asterisks - I’ll get to those in a second.

Below the coefficient estimates, we have our measures of precision, in parentheses.215 Some regression tables put the precision measures to the right of the coefficient rather than below, so you’d have two columns for each regression. In particular, in this table these are the standard errors of the coefficients. \(se(\hat{\beta}_1)\) in this regression is \(.0004\) - seems pretty precise to me. There are a few different ways you can measure the precision of a coefficient estimate. Putting standard errors here is the most common, but sometimes you’ll see something like a confidence interval. In some fields, using a t-statistic (coefficient divided by the standard error) is more common than the standard error. Ideally a table will tell you which one they’re doing, but not always!216 If it doesn’t say, it’s usually a standard error, and if it’s a single number it’s almost always a standard error or a t-statistic. You can tell which of those two it is by looking at the significance stars - if precision values that are big relative to their coefficients give you significance, that’s probably a t-statistic. If small values relative to the coefficients give you significance, that’s probably a standard error.

Finally, we have those asterisks, called “significance stars.” These let you know at a glance whether the coefficient is statistically significantly different from a null-hypothesis value of 0. To be really precise, these aren’t exactly significance tests. Instead, they’re a representation of the p-value.217 Remember, the p-value is the probability of being as far away from the null hypothesis value (or farther) as our estimate actually is. If the p-value is below \(\alpha\), that’s statistical significance. The lower the p-value is, the more stars we get.

Which p-value cutoff each number of stars corresponds to changes from field to field but should be described in the table note as it is here. A standard in many of the social sciences, and what you’ll see in this book, is that * means that the p-value is below .1 (10%), ** means it’s below .05 (5%), and *** means it’s below .01 (1%).218 In many fields, and in most R commands by default, everything is shifted over one step. * is below .05, ** is below .01, and *** is below .001. There’s often another indicator in these cases like + for .1. So if we see *** as we do in this table for the coefficient on Number of Locations, that would mean that if we had decided that \(\alpha = .01\) (or higher), we would reject the null of \(\beta_1 = 0\). If we see ** then we’d find statistical significance at \(\alpha = .05\) or higher. Basically, it’s a measure of which \(\alpha\) values you’d find significance with for this coefficient.219 This is a bit backwards - we generally want to choose a \(\alpha\) value before we start. What’s the point of knowing significance tests at higher \(\alpha\) values? We already said that doesn’t count. And if our \(\alpha = .05\), then *** doesn’t really give us additional information - something is either significant or it’s not. There’s no such thing as “more significant.” Of course, I’m describing an idealized version of significance testing that people don’t actually do. These stars are a way of, at a glance, being able to tell which of the coefficients are statistically significantly different from 0, which all of these are.

Moving down the table, we have a bunch of things that aren’t coefficients or precision measures. Which of these exact statistics are present will vary from table to table,220 Some other common appearances here might be an information criterion or two (like AIC or BIC, the Akaike and Bayesian Information Criterion, respectively) or the sum of squares. I won’t be covering these here. but in general these are either descriptions of the analysis being run, or measures of the quality of the model. For the first, it’s common to see any additional details about estimation listed down here (such as any standard error adjustments), and just about every table will tell you the number of Observations (or sometimes “N”) included in estimating the regression.

For the second, there are a billion different ways to measure the quality of the model. Probably two of the most common are included here - \(R^2\) and Adjusted \(R^2\). These are measures of the share of the dependent variable’s variance that is predicted by the model. \(R^2\) in the first model is \(.065\), telling us that 6.5% of the variation in Inspection Score is predicted by the Number of Locations. If we were to predict Inspection Score with Number of Locations and then subtract out our prediction, we’d be left with a residual variable that has only \((100 - .065 = )\) 93.5% of the variance of the original. Adjusted \(R^2\) is the same idea, except that it makes an adjustment for the number of variables you’re using in the model, so it only counts the variance explained above and beyond what you’d get by just adding a random variable to the model.221 Yes, adding a random variable to the model does explain more of its variation. In fact, adding any variable to a model always makes the \(R^2\) go up by some small amount, even if the variable doesn’t make any sense.

Finally, we have the “F-statistic.” This is a statistic used to do a hypothesis test. Specifically, it uses a null that all the coefficents in the model (except the intercept/constant) are all zero at once, and tests how unlikely your results are given that null. It’s pretty rare that this will be insignificant for any halfway-decent model, and so I for one mostly ignore this statistic.

Missing from this particular table, but present in a number of standard regression-table output styles, is the residual standard error, sometimes also called the root mean squared error (RMSE). This is, simply, our estimate of the standard deviation of the error term based on what we see in the standard deviation of the residuals. We take our predicted Inspection Score values based on our OLS model and subtract them from the actual values to get a residual. Then, we calculate the standard deviation of that residual and make a slight adjustment for the “degrees of freedom” - the number of observations in the data minus the number of coefficients in the model. The bigger this number is, the bigger the average errors in prediction for the model are.

What can we do with all of these model-quality measures? Take a quick look, but in general don’t be too concerned about these. These are usually measures of how well your dependent variable is predicted by your OLS model. But if you’re reading this book, you’re probably not that concerned with prediction. You’re interested in identifying causal effects, and in estimating particular coefficients well, rather than predicting the dependent variable overall.

If your \(R^2\) or adjusted \(R^2\) values are low, or your residual standard error is high, what this tells you is that there’s a lot going on with your dependent variable other than what you’ve modeled. Is that a concern? Maybe. If you thought you wrote down a diagram that explained your dependent variable super well and covered all of the things that cause it, and you chose your model and which variables to control for based on that… and then you got a tiny \(R^2\) anyway, then your initial assumption that you really understood the data generating process of your dependent variable might be wrong. But if you don’t care about most of the causes of your dependent variable and are pretty sure you’ve included the variables in your model necessary to identify your treatment, then \(R^2\) is of little importance.

Similar to statistical significance, I see \(R^2\) values as another thing that students tend to fixate on. Gets their buns in a knot.222 I don’t know what this means. But while it can be a nice diagnostic, it’s definitely not something to fixate on. Certainly don’t design your model around maximizing \(R^2\) - build the right model for identifying the effect you want to identify and answer your research question, not the right model for predicting the dependent variable. Even if you are interested in prediction, \(R^2\) has plenty of flaws in use for building predictive models too, although that’s another book.

Knowing where all the pieces of a regression are on a regression table, how can we interpret the results? Let’s take a look at the regression table again in Table 13.3.

| Inspection Score | Inspection Score | |

|---|---|---|

| (Intercept) | 94.866*** | 225.333*** |

| (0.046) | (12.411) | |

| Number of Locations | −0.019*** | −0.019*** |

| (0.000) | (0.000) | |

| Year of Inspection | −0.065*** | |

| (0.006) | ||

| Num.Obs. | 27178 | 27178 |

| R2 | 0.065 | 0.068 |

| R2 Adj. | 0.065 | 0.068 |

| F | 1876.705 | 997.386 |

| RMSE | 6.05 | 6.04 |

| * p < 0.1, ** p < 0.05, *** p < 0.01 |

A key phrase to keep in mind when interpreting the results of an OLS regression is “a one-unit change in…” Regression coefficients are all about estimating a linear relationship between two variables, and reporting the results in terms of the slope, i.e., the relationship between a one-unit change in the predictor variable and the dependent variable.223 Sometimes regression results are presented as “standardized coefficients” for which this becomes “a one-standard-deviation change in…” But you can also just think of it as a “one-unit change” for variables scaled to have a standard deviation of 1.

If we want to get real precise about it, the interpretation of an OLS coefficient \(\beta_1\) on a variable \(X\) is “controlling for the other variables in the model, a one-unit change in \(X\) is linearly associated with a \(\beta_1\)-unit change in \(Y\).” If we want to get even more precise, we can say “If two observations have the same values of the other variables in the model, but one has a value of \(X\) that is one unit higher, the observation with the \(X\) one unit higher will on average have a \(Y\) that is \(\beta_1\) units higher.”

Let’s start with the first column of results, with only one variable, a \(-.019\) on Number of Locations. Let’s think briefly about our units here. Number of Locations is the number of locations in the restaurant chain, and the dependent variable, Inspection Score, is an inspector score on a scale that goes up to 100.

Since we have no other control variables in the model, that \(-.019\) means “a one-unit increase in the number of locations a chain restaurant has is linearly associated with a \(-.019\)-point decrease in inspector score, on a scale of 0-100.” Or, “comparing two restaurants, the one that’s a part of a chain with one more location than the other will on average have an inspection score \(-.019\) lower.”

Notice that however I’m wording it, I’m careful to avoid saying “a one-unit increase in number of locations decreases inspector score by \(-.019\).” This would be implying that I’ve estimated a causal effect. I should only use this language if, based on what we learned in the first part of the book, we think we’ve identified the causal effect of number of locations on inspector score.

How about that constant term 94.866? This is our prediction for the dependent variable when all the predictor variables are zero. Think about it - our conditional mean of the dependent variable is whatever the OLS model spits out when we plug the appropriate values in. If we plug in 0 for everything, it all drops out and all we have left is our constant. So for a restaurant with zero locations, we’d predict an inspector score of 94.866. Of course, it’s impossible to have a restaurant with zero locations, so this doesn’t mean much.224 If you have predictor variables where the relevant range of the data is far away from zero, the constant term can sometimes give strange values. This isn’t a problem - just don’t try to make predictions far outside the range of your data. In general we don’t need to worry ourselves too much about the constant term.

Let’s move to the second column. We’re introducing a control variable here, year of inspection. It doesn’t seem to change the coefficient on number of locations, but it does change the interpretation.

Now we need to incorporate the fact that our interpretation of each coefficient is based on the idea that we are “controlling for” the other variables in the model.225 i.e., closing the back doors that go through those variables. We can say this in a few ways.

We can say “controlling for year of inspection, a one-unit increase in the number of locations a chain restaurant has is linearly associated with a \(-.019\)-point decrease in inspector score, on a scale of 0-100.” Instead of “controlling for” we could instead say “adjusting for” or “adjusting linearly for” or even “conditioning on.”226 Remember the “conditional mean” stuff from Chapter 4? That’s the kind of “conditioning” I mean.

We can say “comparing two inspections in the same year, the one for a restaurant that’s a part of a chain with one more location than the other will on average have an inspection score \(-.019\) lower.” After all, that’s the idea of controlling for variables. We want to compare like-with-like and close back doors, and so we’re trying to remove the part of the Number of Locations/Inspector Score relationship that is driven by Year of Inspection. The idea is that by including a control for Year, we are removing the part explained by Year, and can proceed as though the remaining estimates are comparing two inspections that effectively have the same year. There’s no variation in year left - we have held year constant.227 Or at least we’ve held its linear predictions constant. If Year of Inspection relates to Inspector Score or Number of Locations in ways that are best described by curvy lines, then including Year of Inspection as a linear predictor in the regression equation won’t fully control for it. For this reason you will also often hear the interpretation “holding year of inspection constant, a one-unit increase in the number of locations is associated with a \(-.019\) decrease in inspector score.”

This is a simple guide to interpreting a regression, and one that’s focused pretty heavily on semantics. But training yourself to explain regression in these terms will truly help you interpret them better. The same intuition will carry over when you start doing regression in more complex settings, as we’ll discuss throughout the chapter.

13.1.5 Subscripts in Regression Equations

I’ve left out one common feature of expressing a regression. When writing out the equation for a regression, people will commonly use subscripts on their variables (i.e., \(X_{little text down here}\)). We already have subscripts on our coefficients (the 1 in \(\beta_1\), etc.), but they show up on the variables themselves, too. I’ve chosen mostly to omit these in this book,228 I’ve got nothing against them! But I think at the level we’re working they’re more distracting than helpful. but it’s important to be familiar with the concept when you’re reading papers or writing your own.

A regression might be expressed as

The \(i\) here tells us what index the data varies across. In other words, a single observation is a what exactly? Here we have \(i\), which generally means “individual,” i.e., an individual person or firm or country, depending on context. In this regression, \(Y\) and \(X\) differ across individuals.

Alternately, we might see

The \(t\) here would be shorthand for time period. This is describing a regression where each observation is a different time period. The \(X_{t-1}\) tells us that we are relating \(Y\) from a given period \(t\) to the \(X\) from the period before \((t-1)\).

The subscripts do their best work when there are multiple axes that things could vary along. Consider this example:

This is describing a regression in which \(Y\) and \(X\) vary across a set of individuals \(i\) and across time \(t\) (a panel data set). There is a different intercept for each time period \(\beta_t\), and also a different intercept for each value of \(g\) (and what’s \(g\)? We’d have to look for where the researcher is describing their regression, but it might mean some \(g\)rouping that the individuals \(i\) are sorted into). We also see a control variable \(W_i\). The \(i\) subscript here (and lack of a time subscript \(t\)) tells us that \(W\) only varies across individual and doesn’t change over time. Perhaps \(W\) is something like birthplace that is different for individuals but does not vary over time.

13.1.6 Turning a Causal Diagram into a Regression

Okay, so we’ve covered the basics of how regression works. And we spent the first half of this whole book talking about how to identify causal effects using causal diagrams.

It’s tempting to think that we automatically know how to link the two, but I’ve found that students often have difficulty making this jump. It’s not a super difficult jump, mind you, but it’s not one we can take for granted.

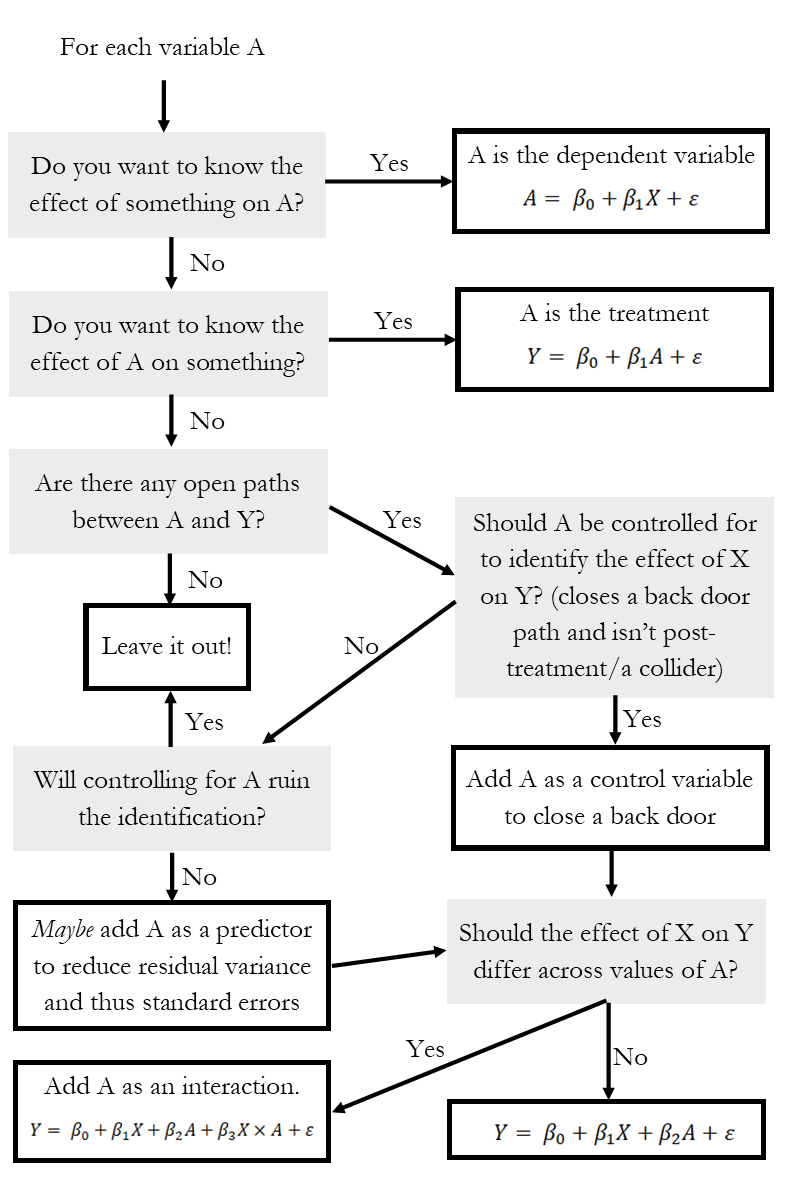

The chart in Figure 13.5 may help. On the diagram, we’re thinking about what to do with a variable \(A\). Is it the outcome variable, or is some other variable \(Y\) the outcome? Is it the treatment, or is some other variable \(X\) the treatment? If it’s neither, where does it go on the diagram and also in a regression, if anywhere at all?

Figure 13.5: Chart for Constructing a Regression Equation

As shown in Figure 13.5, each variable may play one of several roles in a regression. It could be our outcome variable - we know all about those. Outcome variables become the dependent variables in regression, the \(Y=\) part of \(Y = \beta_0 +\beta_1X\). We know all about treatment variables from our discussion of causal diagrams, too. Those become the \(\beta_1X\) part.

How about the rest? Our causal diagram tells us all about variables that need to be adjusted for in order to close back doors (and also those that shouldn’t be controlled for to avoid closing front doors or opening back doors by controlling for colliders). Anything that should be included as a control should be, well, included as a control. That’s the \(+\beta_2A\) part of \(Y = \beta_0+\beta_1X+\beta_2A\), where \(X\) is the treatment and \(Y\) is the outcome.

There are two things we haven’t come to yet that show up in regression but not so much in causal diagrams. First, what if a variable \(A\) doesn’t need to be controlled for, but also controlling for it won’t break the identification? In that case we can include it as a control, and maybe we want to - as long as \(A\) is related to \(Y\), then adding it will explain more of the variation in \(Y\), reducing variance in the error term. And since the standard errors of the regression coefficients like \(\hat{\beta}_1\) rely on the variance of the error term, the standard errors will shrink.

Finally, what about that part of the graph where it asks about whether the effect of treatment will differ across values of \(A\)? That’s where interaction terms come in. We’ll talk about those later in the chapter.

13.1.7 Coding Up a Regression

Before we move on, we should probably actually do a regression. Seems like a good idea.

The following code chunks will replicate Tables 13.2 and 13.3 in R, Stata, and Python. They will load in the restaurant inspection data, calculate the number of locations, regress inspection score on the number of locations, do another regression that also includes year as a control, and then output a regression table to file.

Note that while the code for performing a regression is fairly standard in each language, the process for producing a regression table generally depends on downloadable packages. There are plenty of options for these packages. I’ll be using the modelsummary R package (install.packages('modelsummary')), estout for Stata (ssc install estout), and stargazer for Python when there’s more than one regression to display (pip install stargazer). But some good alternatives include export_summs from the jtools package, or outreg2, regsave, or the Stata 17 exclusive collect in Stata.229 I recognize that estout is probably the better package for Stata regression tables and that’s why I use it here. I’ve heard good things about regsave, but I personally will use outreg2 until the day that I die. You shall pry its arcane syntax, and the head-scratching fact that it is less up-to-date than outreg, from my cold dead fingers.

R Code

library(tidyverse); library(modelsummary)

res <- causaldata::restaurant_inspections

res <- res %>%

# Create NumberofLocations

group_by(business_name) %>%

mutate(NumberofLocations = n())

# Perform the first, one-predictor regression

# use the lm() function, with ~ telling us what

# the dependent variable varies over

m1 <- lm(inspection_score ~ NumberofLocations, data = res)

# Now add year as a control

# Just use + to add more terms to the regression

m2 <- lm(inspection_score ~ NumberofLocations + Year, data = res)

# Give msummary a list() of the models we want in our table

# and save to the file "regression_table.html"

# (see help(msummary) for other options)

msummary(list(m1, m2),

stars=TRUE,

output= 'regression_table.html')

# Default significance stars are +/*/**/*** .1/.05/.01/.001. Social science

# standard */**/*** .1/.05/.01 can be restored with

msummary(list(m1, m2),

stars=c('*' = .1, '**' = .05, '***' = .01),

output= 'regression_table.html')Stata Code

* ssc install causaldata if you haven't yet!

causaldata restaurant_inspections.dta, use clear download

* Create NumberofLocations

by business_name, sort: g NumberofLocations = _N

* Perform the first, one-predictor regression

regress inspection_score NumberofLocations

* Store our results for estout

estimates store m1

* Now add year as a control

regress inspection_score NumberofLocations year

estimates store m2

* use esttab to create a regression table

* note esttab defaults to t-statistics, so we use

* the se option to put standard errors instead

* we'll save the result as regression_table.html

* (see help esttab for other options)

esttab m1 m2 using regression_table.html, se replacePython Code

import pandas as pd

import statsmodels.formula.api as smf

from stargazer.stargazer import Stargazer

from causaldata import restaurant_inspections

res = restaurant_inspections.load_pandas().data

# Perform the first, one-predictor regression

# use the sm.ols() function, with ~ telling us what

# the dependent variable varies over

m1 = smf.ols(formula = 'inspection_score ~ NumberofLocations',

data = res).fit()

# Now add year as a control

# Just use + to add more terms to the regression

m2 = smf.ols(formula = 'inspection_score ~ NumberofLocations + Year',

data = res).fit()

# Open a file to write to

f = open('regression_table.html', 'w')

# Give Stargazer a list of the models we want

# in our table and save to file

regtable = Stargazer([m1, m2])

f.write(regtable.render_html())

f.close()13.2 Getting Fancier with Regression

Regression is a tool - a very flexible tool. And we’ve only really learned one way to use it! This section isn’t even going to change how we use it; it’s just going to change the variables that go into it. This in itself will open up a whole new world.

So far, we’ve talked about regression of the format \(Y = \beta_0 + \beta_1X + \beta_2Z+ \varepsilon\). We’re still working with that. But we’ve also always been working with continuous variables included in the regression as their normal selves. Is there something else?

First, we might not have continuous variables. Instead, we might have discrete variables, which most often pop up as binary variables - true or false, rather than a particular number. How can we interpret \(\beta_2\) if \(Z\) is “this person has blonde hair”? Or, how would we control for “hair color” if that’s not a variable we’ve measured continuously, and we instead have categories like “black,” “brown,” “blonde,” and “red”?

Second, we might not use variables as they are but first transform them. We talked way back in Chapter 4 that some relationships might not be well-described by straight lines. Sometimes we want curvy lines. How can we do that, exactly?

Third, the relationships themselves might be affected by other variables. For example, back in Chapter 4 we talked about a study by Emily Oster that asked “is the relationship between taking vitamin E and health outcomes stronger during the period when vitamin E was recommended by doctors than during the periods when it wasn’t?” We can model the relationship between taking vitamin E and health outcomes with \(Outcomes = \beta_0 + \beta_1VitaminE+\varepsilon\). But how can we model how that relationship changes over time? We need an interaction.

So those three things - all of which have to do with the kinds of variables we use as predictors in our OLS model - will be where we start. Once we’ve covered that, we’ll move on to how we deal with standard errors, and when our dependent variable isn’t continuous either.

13.2.1 Handling Discrete Variables

Binary variables are absolutely everywhere in social science. Did you get the treatment or not? Are you left-handed or right-handed? Are you a man or a woman?230 Some people point out this should not be treated as a binary variable. I hope those people know how hard they’re making regression analysis. Think of the researchers. Are you Catholic or not? Are you married or not?

Binary variables are especially important for causal analysis, since a lot of the causes we tend to be interested in are binary in nature. Did you get the treatment or not?

Any time we have something that you are or are not, which happens any time we have some sort of qualitative description, we are dealing with a binary variable. These can be included in regression models just as normal. So we can still be working with \(Y = \beta_0 + \beta_1X + \beta_2Z+ \varepsilon\), but now maybe \(X\) or \(Z\) (or both) can only take two values: 0 (“are not”/false) or 1 (“are”/true).231 Sometimes you’ll see people use -1 and 1, or 1 and 2, instead of 0 and 1. This is usually just confusing though, and pretty rare in the social sciences. If the binary variable is a control variable, we can think of it as we normally do - we’re just shutting off back doors that go through the variable. But what if we are interested in the effect of that binary variable? How can we interpret the binary variable’s coefficient?

Simply put, it’s the difference in the dependent variable between the trues and the falses.232 Why is this? OLS is trying to fit a line that minimizes squared residuals. But there are only two values the data can take on the \(x\)-axis: 0 and 1. Because of that, the OLS line can only produce two real predictions: one when it’s 0 on the \(x\)-axis, and one when it’s 1. The best prediction you can make in each case, which minimizes the squared residuals is just the mean of the outcome conditional on the binary variable being 0 or 1. Then, the slope of the line is just how much the prediction increases when the \(x\)-axis variable increases by 1 (i.e., goes from 0 to 1). So for example, if we ran the regression \(Sales = \beta_0 + \beta_1Winter + \varepsilon\), where \(Winter\) is a binary variable that’s 1 whenever it’s Winter and 0 when it’s not, then \(\beta_1\) would be how much higher sales are on average in Winter than in Not Winter.233 And if sales are lower on average in Winter, \(\beta_1\) would be negative.

When we estimate the model, if we got \(\hat{\beta}_1 = -5\), then we’d say that, on average, sales are 5 lower in Winter than they are in Not Winter. Take a look at the simulated data in Table 13.4. Notice that the coefficient on Winter (-5) is just the difference between the mean for Not Winter (15) and the mean for winter (10). Also notice that the coefficient on the intercept (15) is the expected mean when all the variables are zero - when Winter is 0, we’re in Not Winter, and average sales in Not Winter are 15.

Table 13.4: Average Sales by Season, or Regression of Sales on Winter

| Mean | OLS Estimates | |

|---|---|---|

| Winter | 10.000 | -5.000 |

| (1.103) | ||

| Not Winter | 15.000 | (Ref.) |

| (Intercept) | 15.000 | |

| (3.413) |

Note: Standard errors are in parentheses. No significance stars are shown.

One important thing to note is that we only include one side of the yes/no question. The model is \(Sales = \beta_0 + \beta_1Winter + \varepsilon\), not \(Sales = \beta_0 + \beta_1Winter + \beta_2NotWinter + \varepsilon\). Why is this? First off, imagine trying to interpret that. We want \(\beta_1\) to compare Winter to Not Winter, but \(\beta_2\) compares Not Winter to Winter. So… what’s the difference between them? Interpretation would be pretty confusing. Second, this is to satisfy another OLS assumption we have to make, that there is no perfect multicollinearity. That is, you can’t make a perfect linear prediction of any of the variables in the model with any of the other variables. Here, \(Winter + NotWinter = 1\). We don’t have a 1 in our model, though, so no problem, right? Wrong! There is an all-1s variable lurking in our model at all times—it’s being multiplied by the constant!

Why can’t we have that linear combination? Because OLS wouldn’t be able to figure out how to estimate the parameters. Imagine the average sales in Winter are 10, and in Not Winter it’s 15. If your regression is \(Sales = \beta_0 + \beta_1Winter + \beta_2NotWinter + \varepsilon\), you could generate those exact same predictions with \(\beta_0 = 15, \beta_1 = -5, \beta_2 = 0\). Or with \(\beta_0 = 10, \beta_1 = 0, \beta_2 = 5\). Or with \(\beta_0 = 3, \beta_1 = 7, \beta_2 = 12\). Or any infinite number of other ways! And while they’d all work, OLS has no way of picking one estimate out of those many, many options. It can’t give you a best estimate any more. We need to limit its options by dropping NotWinter, in effect forcing it to choose the \(\beta_0 = 15, \beta_1 = -5, \beta_2 = 0\) version.

We can expand our intuition about binary variables just a bit and give ourselves the ability to include categorical variables in our model. Binary variables are just yes/no. But categorical variables can take any number of categories. These include variables like “what country do you live in?” or “what decade were you born in?” You can’t answer these questions with yes and no, but they are discrete and mutually exclusive categories.234 Sometimes these categories might allow some overlap - some people do live in multiple countries, for example. But hopefully we can avoid these situations, or there are few enough of them we can just ignore them, as they make things much more difficult.

We can handle categorical variables by just giving each of the categories its own binary variable. So instead of one variable for “which country do you live in?” it’s one variable for “do you live in France?”, another for “do you live in Gambia?”, another for “do you live in New Zealand?” and so on. \(Income = \beta_0 + \beta_1France + \beta_2Gambia+ \beta_3NewZealand + ...\) If we’re including the categorical variable as a control, by including these binary variables for each category we can say that we’ve closed the back doors that go through, in this example, which country you live in.

And what if we want to interpret the coefficient on one of these binary categories? This is just a hair trickier than with a binary variable. Just like we couldn’t include both sides of the binary variable in the model (we had to put just Winter in the model, not Winter and NotWinter), we also can’t include every single category in the model. We need to drop one of them. The one we drop then becomes the “reference category.” All the coefficients are relative to that category.

Before, with binary variables, the coefficient gave the difference between “yes” and “no.” Now, with a categorical variable and a reference category, it’s the difference between “this category” and “the reference category.”

For example, if we drop France from our regression,235 This does not mean we’re dropping all the observations from France. It just means we’re removing the \(France\) binary variable from our regression. France becomes the reference category. If we then estimate \(Income = \beta_0 + \beta_1Gambia+ \beta_2NewZealand + ...\) and get \(\hat{\beta}_1 = .5\) and \(\hat{\beta}_2 = 3\), then that means average income in Gambia is .5 higher than average income in France and average income in New Zealand is 3 higher than average income in France. Both of the interpretations only take things relative to the reference category, not each other.

We can see this in the simulated data in Table 13.5, which includes data only for France, Gambia, and New Zealand. Notice that average income for Gambia (30.5) is \(.5\) higher than the average income for France (30), and the coefficient on Gambia when France is the reference category is \(.5\). Similarly, the average income for New Zealand (33) is 3 higher than France, and the coefficient is 3. The intercept is the average income when all the predictors are 0 - so it’s not Gambia, and it’s not New Zealand, meaning it must be France. The average income in France is 30, so the intercept is 30.

Table 13.5: Average Income by Country among France, Gambia, and New Zealand, or Regression of Income on Country

| Mean | OLS Estimates | |

|---|---|---|

| France | 30.000 | (Ref.) |

| Gambia | 30.500 | .500 |

| (.103) | ||

| New Zealand | 33.000 | 3.000 |

| (1.321) | ||

| (Intercept) | 30.000 | |

| (5.412) |

Note: Standard errors are in parentheses. No significance stars are shown.

This reference category stuff means that the coefficients on the categories (and their significance) have relatively little meaning on their own. They only have meaning relative to each other. The coefficients change completely if you change the reference category. If we made New Zealand the reference category instead, the coefficient on Gambia would change from .5 to -2.5.236 Can you spot why?

If you want to know whether a categorical variable has a significant effect as a whole, you don’t look at the individual coefficients. Instead, you look at all the category coefficients. This takes the form of a “joint F test,” where you compare the predictive power of the model against a version where the categorical variable has been removed as a predictor.

In R, the linearHypothesis command in the car package can perform the joint F test. You give it the full list of names of coefficients for the categories (which you can make yourself using paste and unique with a little effort, or the matchCoefs() function). Slightly easier to use is wald() in the fixest package, which lets you easily pattern-match variable names, although this also requires the use of fixest’s feols() regression function instead of lm(). In Stata, testparm i.cat will do a joint significance test of all the categories of the cat variable. In Python, if you use smf.OLS().fit() to create a regression results object, let’s say it’s called m1, then you can do a joint F test with m1.f_test(). You’ll need to read the documentation to see how to create a matrix or string indicating the factor variables to be tested.

13.2.2 Polynomials

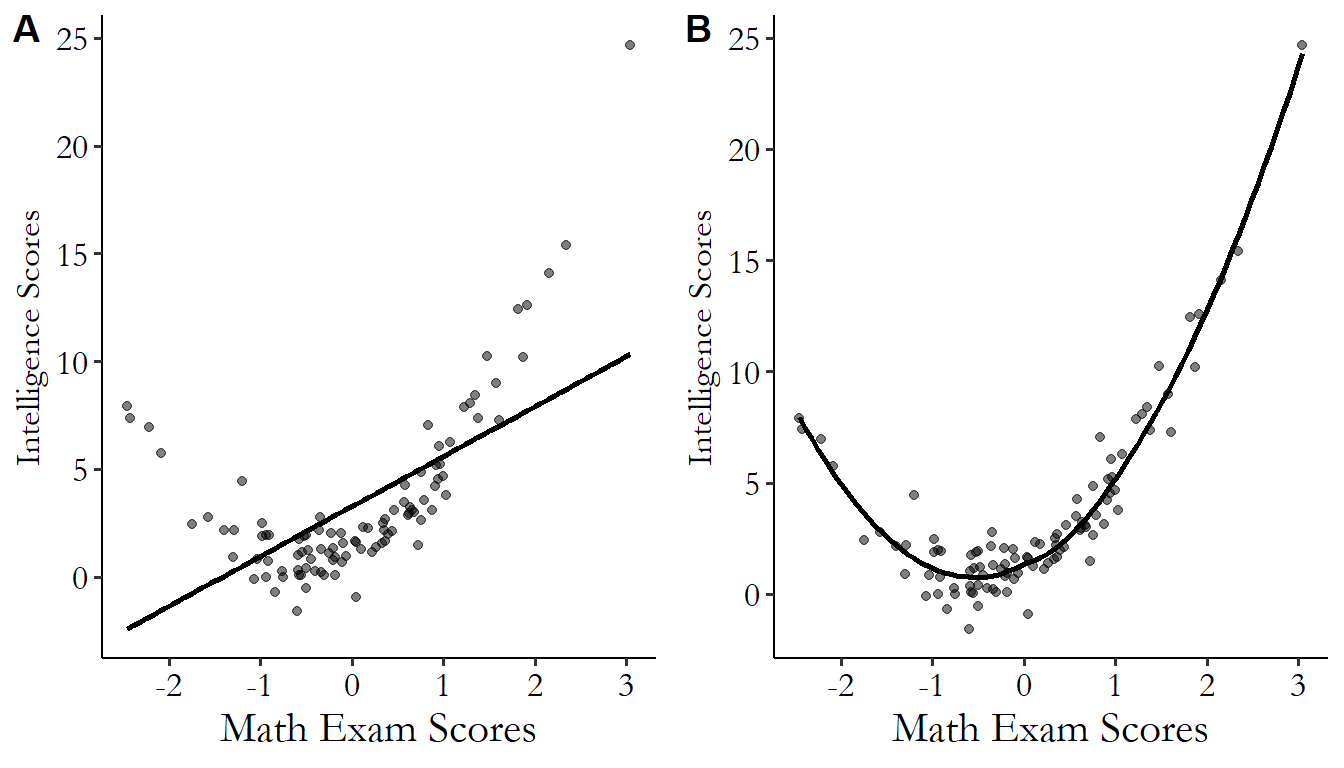

Sometimes, a straight line isn’t enough. OLS assumes that the relationship between the dependent variable and each of the predictor variables can be described as a straight line (linear). If that’s not true, OLS will do a poor job. For example, look at Figure 13.6. The true relationship clearly follows the curvy line drawn on the right. If we try to estimate this relationship using a straight line, we get something that doesn’t fit very well, shown by the line on the left.

Figure 13.6: Math Scores and Intelligence: OLS and the True Model

We can still use OLS for these kinds of relationships though. We just need to be careful to model that curviness right in our regression equation.

There are two main ways we can do this: we can either add polynomial terms, or we can transform the data.

A polynomial is when you have the same variable in an equation as itself, as well as powers of itself. So for example, \(\beta_1X + \beta_2X^2 + \beta_3X^3\) would be a “third-order polynomial” since it contains \(X\) to the first power (\(X\)), the second power (\(X^2\)), and the third power (\(X^3\)).237 These are also referred to as the linear, squared, and cubic terms, with quartic for the fourth power. \(^,\)238 Notice that this contains all the terms up to the third power. You pretty much never want to omit any, as in \(\beta_1X^2 + \beta_2X^3\) which has the second- and third-order terms but not the first.

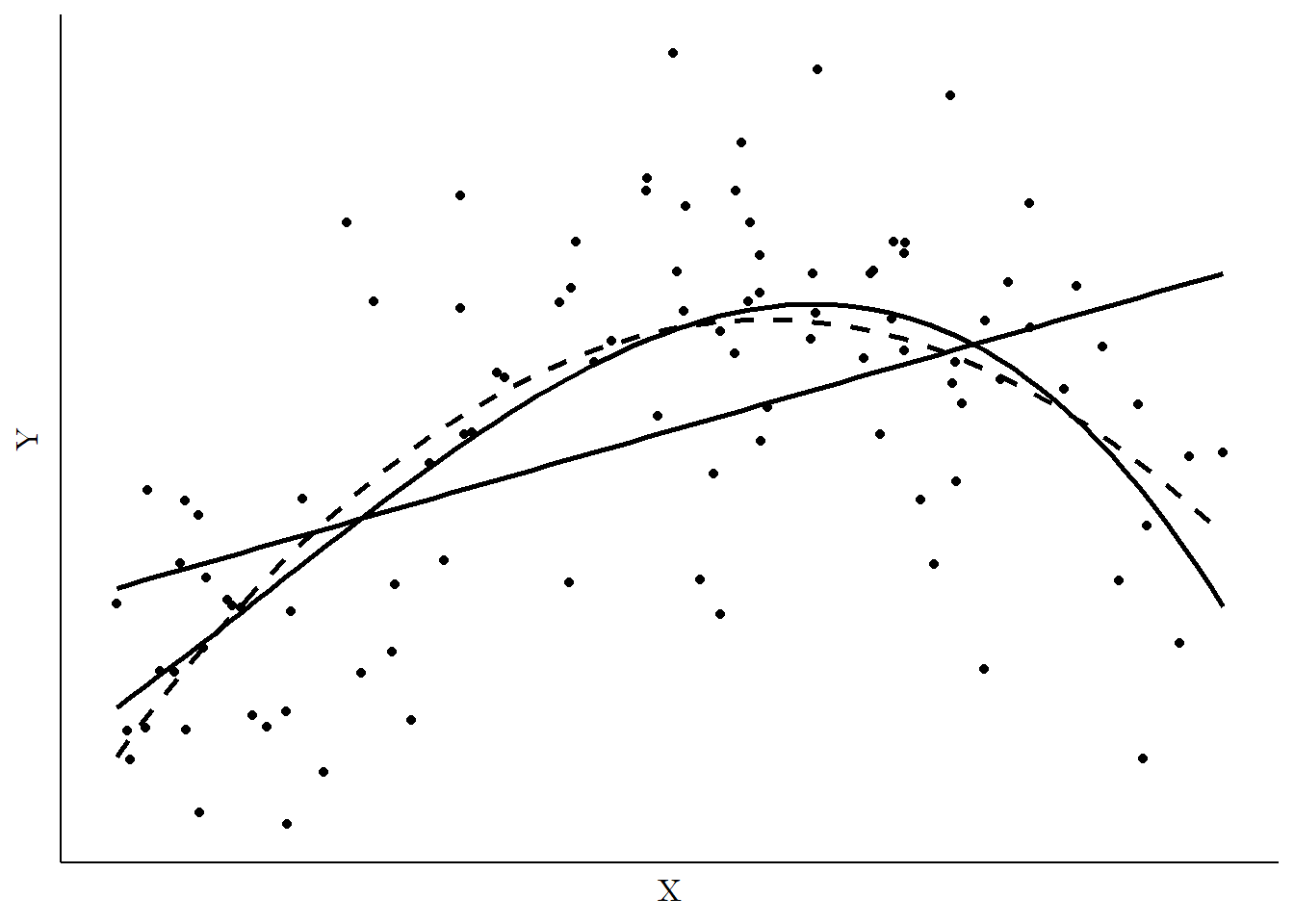

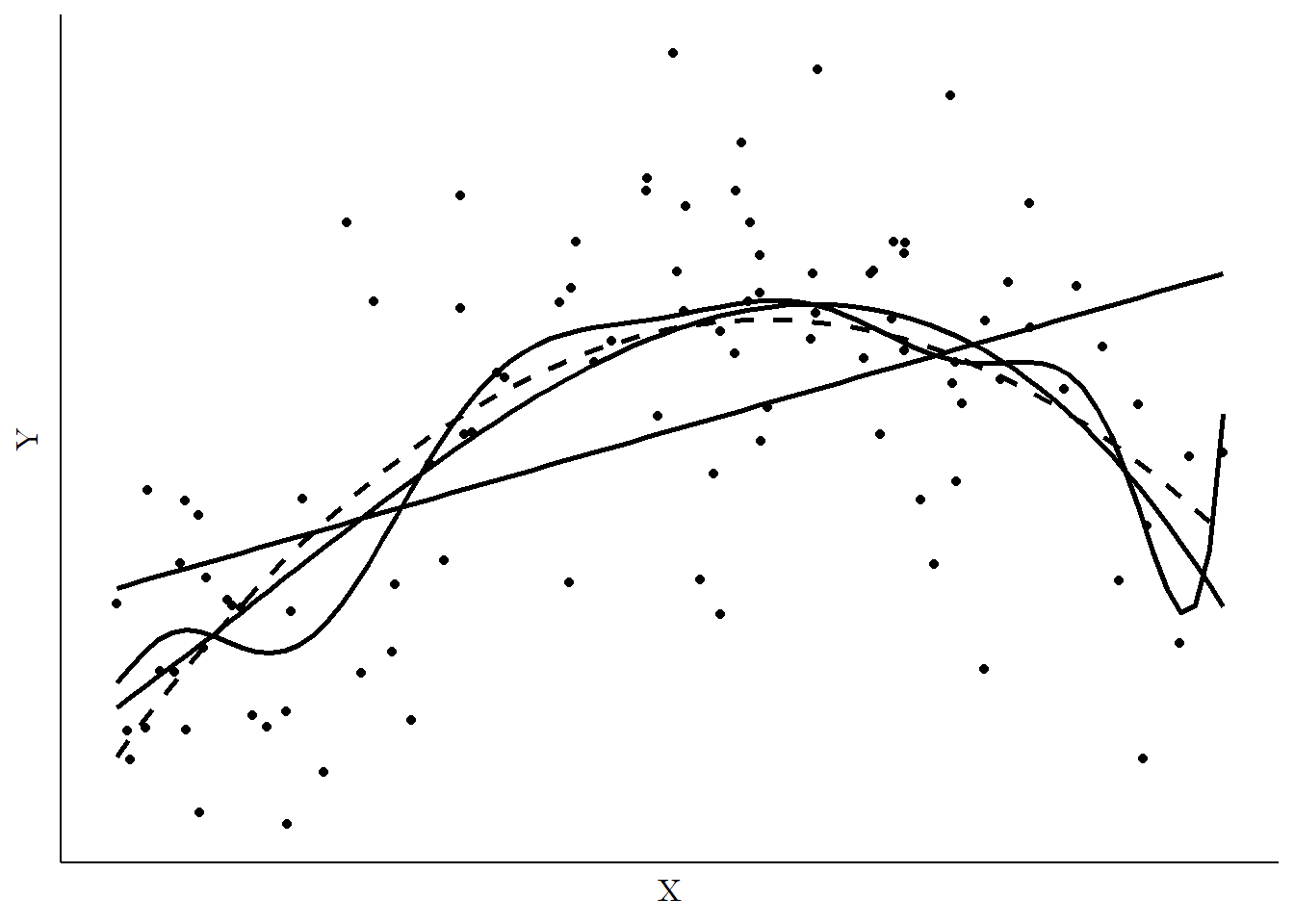

By adding these polynomial terms, it’s possible to fit lines that aren’t straight. In fact, add enough terms and you can mimic just about any shape.239 Any functional relationship, that is - it still needs to make sense that we’re trying to get a single conditional mean of \(Y\) for each value of \(X\). This can be seen in Figure 13.7. Looking at the data points directly, this is clearly a nonlinear relationship. On top of the data points we have the best-fit line from a linear model (\(Y = \beta_0 + \beta_1X\)), which gives the straight line, a second-order polynomial model, which gives the curvy dashed line (\(Y = \beta_0 + \beta_1X + \beta_2X^2\)), and a third-order polynomial, which gives the curvy solid line (\(Y = \beta_0 + \beta_1X + \beta_2X^2 + \beta_3X^3\)).

Figure 13.7: Regression Using a Linear, Square, and Cubic Model

The curvy lines clearly do a better job fitting the relationship, and all we had to do was add those polynomial terms!

That’s the reason to add polynomial terms then. Add polynomial terms and you can better fit a line to a non-straight relationship. But this leaves us with two pressing questions: (1) how can we interpret the regression model once we have polynomial terms, and (2) why not just add a bunch of polynomial terms all the time?

How can we interpret a model with polynomials? For this one, we’re going to need a little calculus, I’m afraid. Let’s take our cubic model from before:

Our typical interpretation of a regression coefficient estimate like \(\hat{\beta}_1\) would be “holding everything else constant, a one-unit increase in \(X\) is associated with a \(\hat{\beta}_1\)-unit increase in \(Y\).” However, that’s a problem! We can’t “hold everything else constant” because there’s no way to change \(X\) without also changing \(X^2\) and \(X^3\). So an interpretation of the effect of \(X\) must take into account the coefficients on each of its polynomial terms. When a regression model includes a polynomial for \(X\), the individual coefficients on the \(X\) terms mean very little on their own, and must be interpreted together.

How can we interpret them together? Let’s try to get back our interpretation of “holding everything else constant, a one-unit increase in \(X\) is associated with a (???)-unit increase in \(Y\).” What is (???)? Well, what tool can we always reach for to figure out how one variable changes with another? The derivative! If we take the derivative of \(Y\) with respect to \(X\), that will tell us how a one-unit change in \(X\) is related to \(Y\).240 This works in a linear model too, of course. In \(Y = \beta_0 + \beta_1X\), the derivative of \(Y\) with respect to \(X\) is just \(\beta_1\). And thus we have our standard interpretation of \(\beta_1\) from a linear model.

A one-unit change in \(X\) is associated with a \((\beta_1 + 2\beta_2X+ 3\beta_3X^2)\)-unit change in \(Y\).241 Even if you don’t know calculus, if all you’ve got is a polynomial, this is a derivative that’s easy enough to do yourself. Just take each term, multiply it by its exponent, and then subtract one from the exponent (keeping in mind that \(X = X^1\), and when you subtract one from that exponent you get \(X^0 = 1\)). So \(\beta_3X^3\) gets multiplied by its exponent of 3 to get \(3\beta_3X^3\), and then we subtract one from the exponent to get \(3\beta_3X^2\). Repeat with each term. Notice that the relationship varies with different values of \(X\). If \(X = 1\), then the effect is \(\beta_1+ 2\beta_2+ 3\beta_3\). But if \(X = 2\), then it’s \(\beta_1 + 4\beta_2 + 12\beta_3\). The effect of \(X\) on \(Y\) depends on the value of \(X\) we already have. This is what we’d expect. Look back at Figure 13.7 - as \(X\) increases, at first \(Y\) increases as well, but then \(Y\) stops increasing and starts declining. The effect of a one-unit change in \(X\) should vary as we move along the \(X\)-axis.

Let’s use a more concrete example. Let’s go back to our regression from Table 13.2 but add a squared term, which we can see in Table 13.6.

| Inspection Score | |

|---|---|

| Constant | 97.5179*** |

| (0.0588) | |

| Number of Locations | −0.0802*** |

| (0.0010) | |

| Number of Locations Squared | 0.0001*** |

| (0.0000) | |

| Num.Obs. | 27178 |

| R2 | 0.194 |

| R2 Adj. | 0.194 |

| F | 3279.008 |

| RMSE | 5.62 |

| * p < 0.1, ** p < 0.05, *** p < 0.01 |

Here we see a coefficient of \(-.0802\) on the linear term, and \(.0001\) on the squared term. This means that a one-location increase in the number of locations associated with a restaurant chain is associated with a \(\beta_1 + 2\beta_2NumberofLocations\), or \(-.0802 + .0002NumberofLocations\), change in the health inspection score. So for a chain with only one location, adding a second one would be associated with a \(-.0802 + .0002(1) = -.0800\) reduction in the health score. But for a chain with 1000 locations, adding its 1001st would be associated with a \(-.0802 + .0002(1000) = .1198\) increase in its health score. There is no single effect; it depends on what part of the \(X\)-axis we’re on. Leaving out the squared term would ignore that.

Polynomials seem pretty handy! So why not just add a whole bunch of them all the time? And while we’re at it, why stop at just square terms and cubics? Why not add four-, five-, six-, or seven-order polynomials to all our models?

There are a few good reasons. For one, the model does get a little harder to interpret. Of course, if it’s the right model we’d still want that anyway.

For another, often the higher-order polynomial terms don’t really do anything. Take Figure 13.7 for example. The line fits from the second-order polynomial and the third-order polynomial models are almost exactly the same.242 And I can tell you, since I generated this data myself, that the true underlying model actually does have a cubic term. Despite this, the cubic term in the regression adds little to nothing. So in many cases, by adding more and more polynomial terms, you make your model more complex without actually improving its fit.

There is also the issue that adding polynomial terms puts strain on the data and can lead to “overfitting,” where a too-flexible model winds up bending in strange shapes to try to fit noise in the data, producing a worse model. Imagine, for example, fitting a 100-order polynomial on a data set with 100 observations in it. We’d predict every point perfectly, but clearly that line isn’t really going to tell us much of anything.

Adding more polynomial terms can, in general, make the model very sensitive to little changes in the data and can make its predictions kind of strange near the edges of the observed data. Take Figure 13.8, for example, which starts with Figure 13.7 and adds a regression fit using a ten-degree polynomial. The shape doesn’t seem to follow the data all that much better than even the two-order polynomial. And we get strange up-and-down motion that seems to chase individual observations rather than the overall relationship. The worst offender is over on the far right, where at the last moment the line springs way up to try to fit the single point on the far right of the data. Those additional degrees in the polynomial aren’t just unnecessary, they’re actively making the model worse.

Figure 13.8: Regression Using a Linear, Square, Cubic, and Ten-degree Polynomial Model

So we don’t want “too many” polynomial terms. But how much is just right? Well, ideally, you want to have the number of polynomial terms necessary to model the actual true underlying shape of the relationship. But we don’t actually know what that is, so that doesn’t help much.

A good way to approach the question of how many polynomial terms to include (or whether to include them at all) is graphically. This works best when you don’t have too many observations. Just draw yourself a scatterplot and see what the shape of the data looks like. Then, add your regression line and see whether it seems to explain the shape you see. If it doesn’t, try adding another polynomial term until it does.

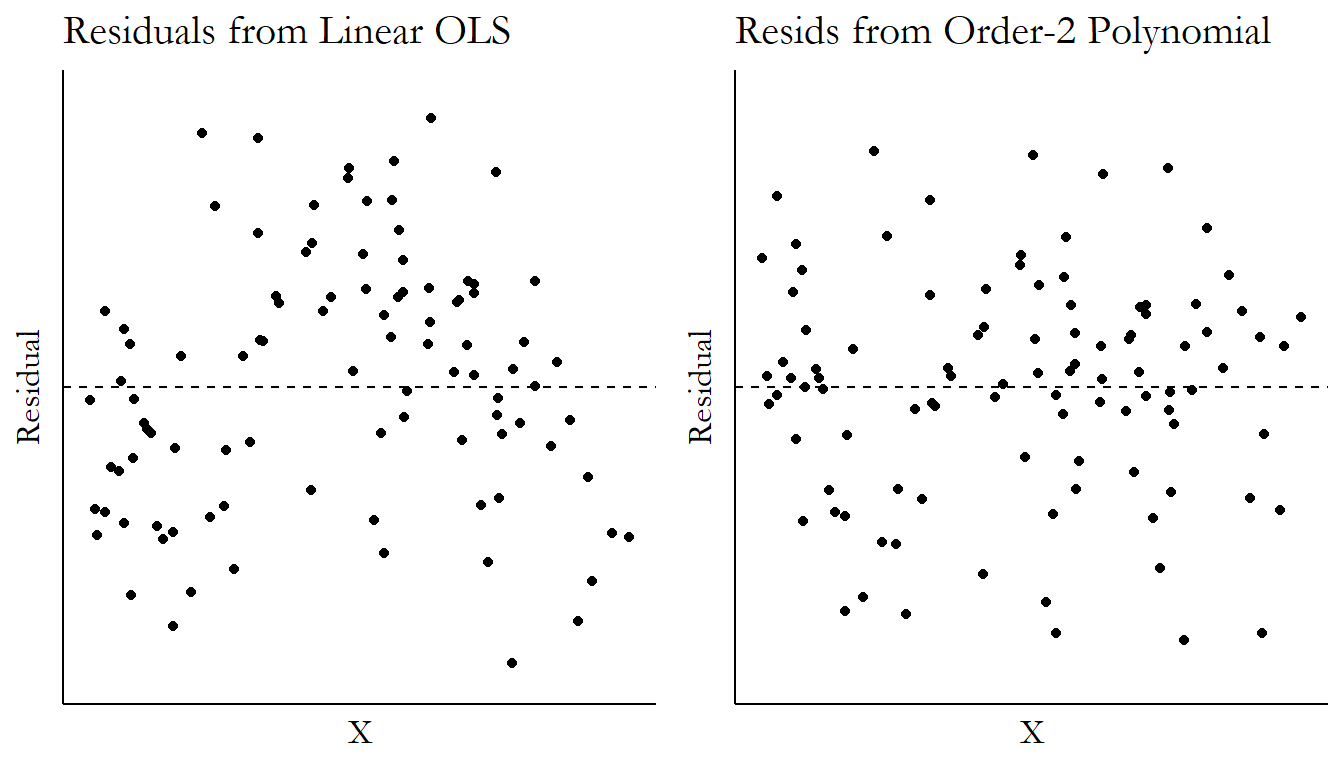

You can also graphically analyze the residuals. Try a regression model, calculate the residuals, and then plot those on the \(y\)-axis against your \(x\)-axis variable. If you have enough polynomial terms, there shouldn’t be any sort of obvious relationship between \(X\) and the residuals. This can be seen in Figure 13.9. The same data from Figure 13.8 is estimated using a linear OLS and a second-order polynomial OLS, and the residuals from those regressions are plotted against \(X\). After the linear regression, there’s still a clear shape to the relationship between the residuals and \(X\) on the left. Not enough curviness to our line. But on the right, after our second-order polynomial, it’s just a bunch of noise around 0. That’s enough, we can stop!